Understanding the Implications of SB 253 on Corporate Emissions Disclosures

What is SB 253?

SB 253 is a California law targeting corporate greenhouse gas (GHG) emissions reporting. It mandates U.S.-incorporated entities with annual revenues exceeding $1 billion and doing business in California to disclose their total GHG emissions. This regulation aims to increase transparency around corporate emissions and drive accountability for climate impacts.

Identifying SB 253-Eligible Firms

Data Sources

To identify firms eligible under SB 253, we leverage data from S&P Global Sustainable1, previously known as Trucost. They provide insights into corporate GHG emissions based on disclosures from companies or model-based estimates when needed. The Sustainable1 emissions data is aligned with the GHG Protocol’s reporting boundaries. Our verification process incorporates emissions data from other providers, including MSCI and Refinitiv/LSEG.

Eligibility Criteria

A key consideration is that SB 253 applies to entities with global annual revenues exceeding $1 billion. The law extends its reach based on total revenue, not just revenue generated in California, thus broadening its impact beyond state borders. The California Air Resources Board defines “doing business in California,” indicating that any transaction aimed at financial gain qualifies, provided specific conditions are met.

Current Findings

We identified 2,427 SB 253-eligible firms from the Sustainable1 dataset. This list illustrates that while SB 253 starts in California, it has a considerable impact across the nation. Analysis reveals that major states like California, Texas, and New York contribute significantly to the count of eligible firms.

Emissions Profile of SB 253 Firms

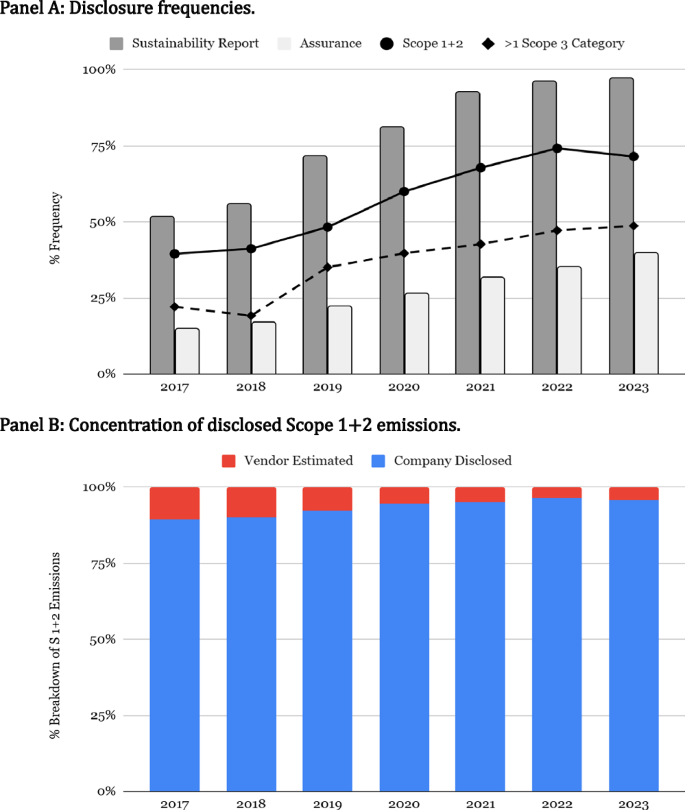

The emissions profile indicates that between 2017 and 2023, Scopes 1 and 2 emissions accounted for only 14% of total emissions from SB 253-eligible firms, while Scope 3 emissions dominated at 86%. This disparity highlights the considerable influence of supply chains and downstream activities on corporate emissions.

Sectoral Differences

Sector analysis reveals that emissions vary significantly:

- The Utilities sector sees about 60% of emissions come from Scopes 1 and 2.

- Meanwhile, sectors like Technology and Finance report over 90% of their emissions as Scope 3, underscoring the necessity for full-scope emissions reporting.

Implications of SB 253 on Compliance Costs

Initial Trends

Data indicates that the percentage of SB 253-eligible firms releasing sustainability reports has surged from 52% in 2017 to 97% by 2023. Though many firms have made progress in disclosing Scopes 1 and 2 emissions, compliance with Scope 3 disclosure requirements could result in substantial costs.

Future Requirements

As disclosure mandates ramp up, firms will need to increase the quality and frequency of their emissions reporting, particularly concerning Scope 3 emissions. This will not only demand internal resources for data collection and management but also necessitate comprehensive assurance processes to align with legislative requirements.

Transitioning to Full Carbon Metrics

As investors increasingly prioritize carbon data in portfolio construction, shifting from partial (Scopes 1 and 2) to full-scope (Scopes 1, 2, and 3) metrics will significantly reshape how carbon performance is assessed. Understanding how this transition impacts sector-peer evaluations can help inform investment strategies.

The Shift in Carbon Performance Metrics

Research shows that moving to full carbon intensity metrics can lead to significant reshuffling in sector rankings. A marked difference in emissions mix among firms complicates direct comparisons, fostering a competitive environment where businesses prioritizing comprehensive emissions reporting can gain a competitive edge.

Portfolio Adjustments and Capital Flows

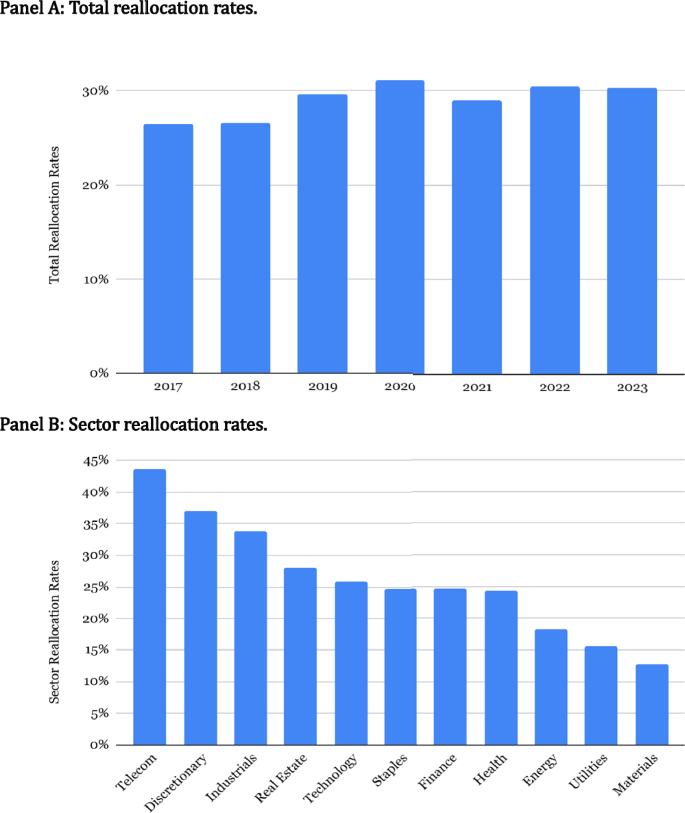

Investors aiming for “best-in-class” companies are likely to benefit from a reallocation of capital as firms adjust their practices to comply with SB 253. We see that the total reallocation rate could be approximately 29%, translating to heightened investment activity in firms demonstrating stronger performance metrics concerning their carbon footprint.

Conclusion

The implications of SB 253 reach beyond California, aiming to reshape corporate transparency regarding emissions. By enhancing disclosures, promoting accountability, and encouraging responsible investment strategies, SB 253 represents a significant shift in how businesses address their environmental responsibilities.

Through ongoing analysis, it becomes clear that as firms adapt to these new standards, both their market positions and environmental impacts will evolve—offering investors a clearer understanding of the carbon footprint associated with their portfolios.

For more information on California’s GHG reporting requirements and the evolving landscape of corporate emissions data, visit California Air Resources Board and S&P Global Sustainability.